Over at The Corner, Avik Roy is outraged at today’s estimate from the CBO that the 2011 deficit will be $1.5 trillion. Beyond the outrage, though, he also implies that perhaps this reflects badly on the CBO’s forecasting ability, since they predicted a lower deficit last year. “What’s a $500 billion, 50 percent error among friends?” he sneers. ZOMG!

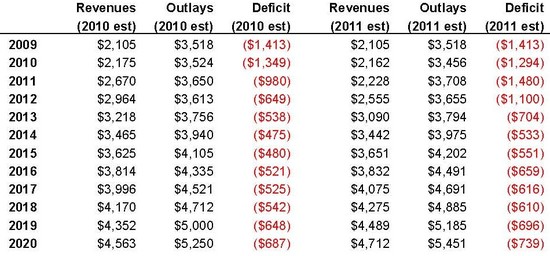

To his credit, though, Roy reproduces a table showing exactly where the $500 billion “error” comes from. Here it is:

Hmmm. Estimated 2011 revenues are down $442 billion, accounting for virtually all of the difference. And where does that come from? Table A-1 in the CBO report provides the answer: nearly all of it is due to the package of tax cuts that were signed into law during the lame duck session last year. Almost none of it is due to technical changes.

So there’s no “error” here. The CBO did fine. What happened was that Congress passed a whole bunch of tax cuts — cuts that I’m sure Roy supported — and those cuts increased the deficit. Only a conservative could possibly be surprised by this. Or someone trying his best to undermine the credibility of the CBO for unrelated reasons. Like, say, someone who doesn’t like the CBO’s contention that healthcare reform will reduce the deficit.

By the way, did I mention that Roy mostly writes about healthcare reform?

UPDATE: Roy responds here. He’s right that not all of the lost revenue comes from extension of the Bush tax cuts. The tax package passed during the lame duck session includes both extension of the Bush tax cuts and various other tax cuts implemented at the same time (the AMT patch, payroll tax holiday, etc.). I’ve corrected the text.