If the United States defaults on its debt, its credit rating will be downgraded catastrophically by every ratings agency. That’s not going to happen because the United States isn’t going to default, but Standard & Poor’s has warned that it might downgrade U.S. debt regardless. Even if there’s no default, says S&P, it might take action if Congress fails to credibly cut the long-term deficit by $4 trillion.

So how worried should we be about this? The answer comes from two places. First this from Time’s Massimo Calabresi:

S&P is an outlier among the top three ratings agencies: Moody’s and Fitch say they won’t even consider a downgrade unless there’s a danger of an actual default.

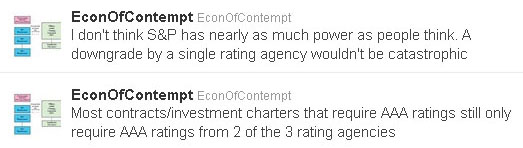

And this from the mysterious Wall Street lawyer who writes Economics of Contempt:

So even if S&P follows through on its threat — and frankly, I suspect it’s just a bluff — it probably won’t have any immediate effect on the market for U.S. bonds. Pension funds won’t have to engage in a massive sell-off, state and local bonds will be fine, and life will go on.

In other words, the threat of actual default is nil, and the threat of downgrade is pretty close to nil too. This goes a long way toward explaining why bond markets aren’t panicking over the debt ceiling fight.

The real danger, of course, is different: shutting down the government for any extended period would likely have a disastrous effect on our still weak economy. Unfortunately, keeping the government operating at the cost of passing the deficit deals currently on the table would probably also be pretty disastrous. We are, for no good reason, deliberately setting our economy on fire. It’s insane. Nero may have fiddled while Rome burned,1 but at least he didn’t set the fire himself.2

1Though probably not, actually.

2Then again, he might have.