Tyler Cowen writes in Bloomberg today about Donald Trump’s main base of support:

Older white Americans are Donald Trump’s core support group, and that’s relevant to the success of Trump’s rhetoric. Commentators frequently cite globalization and wage stagnation as the economic forces behind recent political shifts, but there is a less heralded force influencing American politics: insufficient savings, most of all for older Americans. For those individuals, the prospect of falling standards of consumption — for the remainder of their lives — means the economy is worse than the GDP growth and unemployment numbers are indicating.

….As for today’s 45-to-69-year-olds, only 36 percent claim to be engaging in net savings. And only 45 percent of all people earning $75,000 to $100,000 a year claim to have net positive savings, as measured in 2012. That helps explain why the typical Trump voter in the Republican primaries earned a relatively high income of about $72,000 a year and still worried about his or her economic future.

It’s not really possible to read minds in order to figure out definitively why older white voters support Trump. But the evidence doesn’t support inadequate savings as a possible reason. For starters, older black and Hispanic voters don’t  support Trump, and their savings are even more inadequate than those of older white voters.

support Trump, and their savings are even more inadequate than those of older white voters.

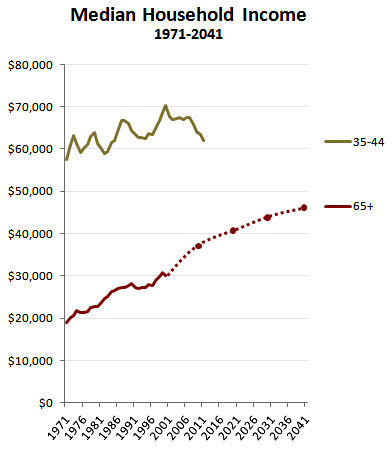

But put that aside and look just at retirement for a moment. Cowen, like most people who write about retirement, offers up a blizzard of scary statistics. But there’s one thing he doesn’t do: put them all together to come up with probable retirement income. However, the Social Security Administration has done this, and their conclusions are clear: retiree income has been rising steadily since the 70s and will continue rising steadily far into the future. This compares to virtually no increase at all for working-age families. When it comes to rising incomes, the 65+ crowd is by far the best-off age cohort in America.

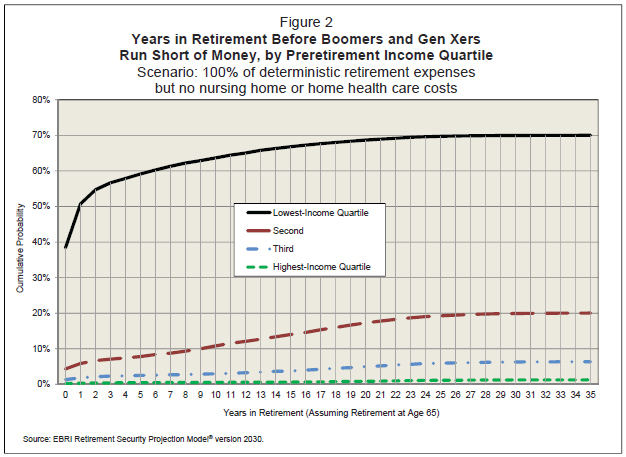

But there’s more. If there’s any group that’s benefited from financial deregulation and the growth of 401(k) plans, it’s higher-income workers. The Employee Benefit Retirement Institute has attempted to take a look at retirement security by income level, and their conclusion is that folks in the top two quartiles—which includes Cowen’s households earning $70-100 thousand per year—are in pretty good shape. Only a tiny fraction are likely to run short of money, even if you go out 35 years:

There are two real retirement risks in America: being poor and ending up in a nursing home. Those are both worth addressing. But overall, Americans are in pretty good retirement shape, and that’s especially true for prosperous families.

So are retirement worries behind the support Trump gets even from affluent older white voters? It’s possible, of course. There’s no telling what people are worried about. But reality doesn’t back it up. Their support for Trump is a lot easier to figure out if you just pay attention to the obvious. That’s not as much fun, but it’s a lot more likely to be correct.