I see that Peter Navarro, one of our many new trade gurus, is taking a break from attacking China and is now attacking Germany. Why? Because it’s unfair that the euro area has lots of weak countries that have collectively produced a weak euro, which gives Germany an advantage in its export business. This is all true enough, and I’m no fan of 21st century German economic policy, but it’s a little pointless right now. The euro isn’t going away, and neither is the fact that Europe’s overall economy is in pretty poor shape.

Still, I’ve been wondering when Germany would come into the crosshairs of the Trump administration. There’s a pretty obvious reason to attack them:

Japan has mostly escaped Trump’s ire for some reason, but I imagine they’re next. After that, I guess Ireland is up to bat. None of this jawboning is likely to do any good, however. As long as the dollar stays strong, we’re going to have trade deficits. And so far it’s staying pretty strong:

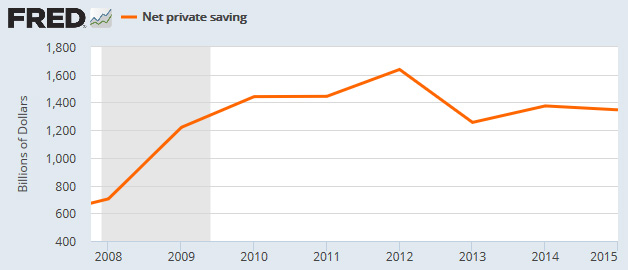

Trump says he wants the trade deficit to decline. This means he wants our trade surplus to increase (from negative to zero), and for that to happen net national savings also have to increase. This is an accounting identity. Now, Trump very plainly has no plans to increase public saving by attacking the budget deficit. In fact, his tax plans will almost certainly explode the deficit to around the trillion dollar territory, which will reduce public saving. This means that private saving would need to increase by a trillion dollars or so for the trade deficit to go away. What are the odds of that?

Trump and his team can blather all they want. But if they want the trade deficit to decline, they need a weaker dollar and higher national savings. Nothing they’re doing points in the direction of either one of those things. Until that happens, it’s all just hot air.