Recently, the go-to argument from the anti-Obamacare forces has been about deductibles. Sure, 20 million people have insurance. Sure, most of them can afford the premiums. But what’s the point if all it buys you is crappy insurance with a $6,000 deductible? As Nathan Nascimento put in National Review a few months ago, “what good is health-insurance coverage for middle- and low-income families if they can’t afford to use it?”

These crocodile tears would be amusing if they weren’t so infuriating. Nobody on the right has ever been willing to support higher funding so that deductibles can come down. In fact, folks on the right love high deductibles. It puts “skin in the game.” A combination of HSAs and high-deductible health policies is one of the standard bits of smoke-and-mirrors offered up by conservatives when you ask them what kind of national health care plan they’d like to see replace Obamacare.

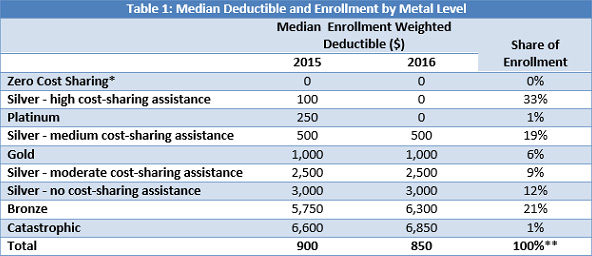

But let’s put that aside for a moment and ask another question: what are the deductibles under Obamacare really like, anyway?1Here’s the answer:

The average deductible decreased from $900 to $850 in 2016. And as you can see if we extrapolate from the figures in the table, it looks like nearly two-thirds of all enrollees had deductibles under $1,000. Only about a fifth had the horror-story $6,000+ deductibles that we hear so much about.

But that’s not all. We don’t have figures for how this breaks down, but my guess is that the majority of the people with high deductibles are the famous “young invincibles” who are single, don’t qualify for subsidies because they’re fairly well off, and don’t think they’re going to get sick. So they buy the cheapest plan they can, take advantage of the preventive care stuff they’re allowed before the deductible kicks in, and go about their lives. No one in their right mind who had any kind of real health issues would ever buy a plan like this.

There are undoubtedly exceptions to this. There always are in a country the size of ours. I’m all for helping these folks out, but one way or another, that calls for more money, not less. Anybody who says otherwise is just playing with you.

1Hat tip to Andrew Sprung, who drew my attention to this table today.