The Senate health care bill takes an axe to Medicaid, but it also does a ton of damage to private insurance purchased on the exchanges. It does this in five ways:1

- Tax subsidies are reduced right out of the gate by changing the benchmark used from “second-lowest cost silver plan” to “applicable median cost benchmark plan.” The “applicable” median plan has an actuarial value of 58 percent, compared to a minimum of 70 percent for a silver plan. This makes it much cheaper, and thus makes the benchmark subsidies lower.

- Subsidies stop entirely at an income of about $42,000, compared to $48,000 currently.

- The age band is increased from 3:1 to 5:1, which will increase premiums for older workers.

- Obamacare’s essential health benefits are eliminated, which allows insurers to offer crappier insurance.

- CSR subsidies are eliminated, which will substantially increase deductibles and copays for poor people.

The end result of all this is that subsidies will go down, coverage will get worse, and deductibles and copays will get higher. Older people will also see an increase in their premiums.

How much does all this add up to? Quite a bit, I’m sure, but we’ll have to wait for the CBO score to put a solid number on it.

1That’s how many I’ve discovered so far, anyway. There are probably other little gems hidden inside the bill that I haven’t caught. I’ll add them to the list when I hear about them.

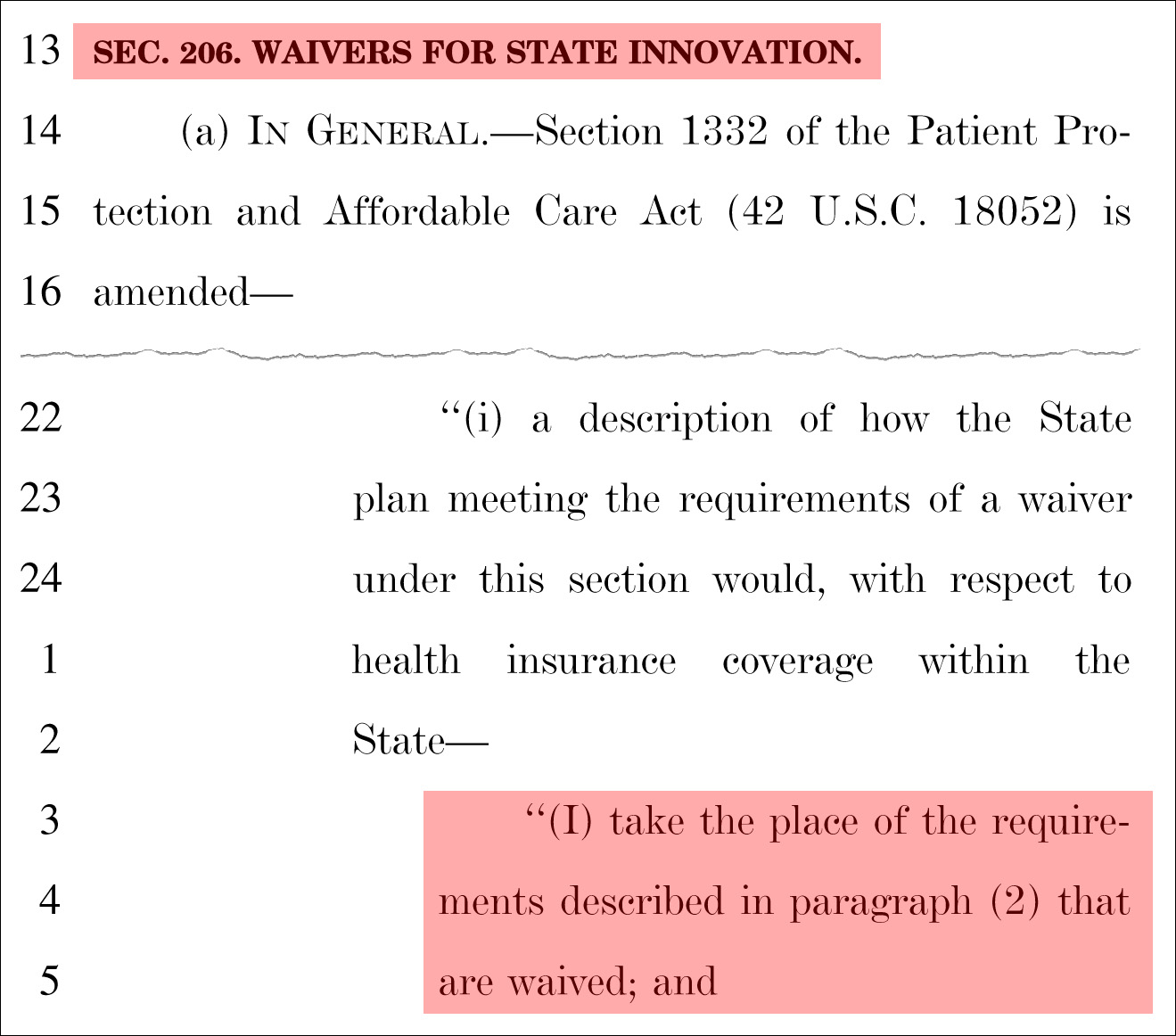

UPDATE: My original post used the wrong excerpt of the bill to illustrate the elimination of essential benefits. It’s actually part of something called a “1332 waiver,” which allows states to apply for an exemption to some of Obamacare’s requirements. Among other things, this exemption can include essential benefits.