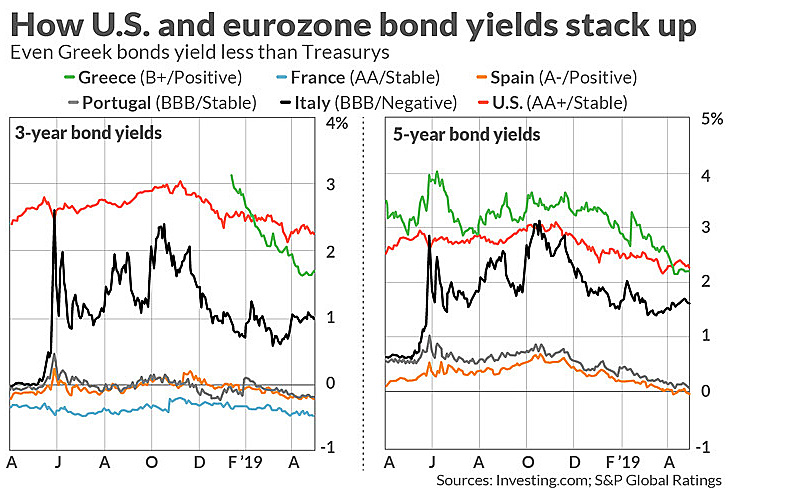

Real interest rates in the eurozone area have been negative for a while. The proximate cause is simple: Eurozone growth is tepid and inflation is subdued, which has caused the European Central Bank to set its policy rate low as a way of stimulating the economy. The current interest rate is -0.5 percent, and once you account for inflation it’s even lower.

This has a different impact in different countries. In Germany, for example, government bond yields are literally negative. In Greece, which is not as economically stable, yields are positive, but only barely: Greek bonds still pay less than US treasurys.

I was cogitating on this the other day and wondering how this could be. The ECB can set interest rates wherever it wants, but it does no good unless people are willing to buy eurozone bonds with low or negative yields. Why, I wondered, would investors accept a lower yield on the Greek bond than on US treasurys? And why are they willing to accept the even lower yields on the bonds of other eurozone governments? It was all above my pay grade, so I googled to get an expert view. Here is Ashoka Mody:

Even if we stipulate that Greece’s government is, in fact, as creditworthy as the U.S. government, why would investors accept a lower yield on the Greek bond? And why are they willing to accept the even lower yields on the bonds of other eurozone governments?

This made me feel better. Even Mody is confused. He offers up a couple of possible reasons for this state of affairs, but concludes that they make no sense. In the end, the question stands. Why would anyone in their right mind accept a lower yield on a Greek bond than a US bond? Or even a German bond, for that matter? Treasurys are the strongest, safest investments around, and the US economy is in better shape than pretty much any European economy.

So: why does anyone buy Greek bonds? Why isn’t there a huge stampede at every auction of Treasurys? Can anyone point me to a nice, simple explainer on this topic?

Can you pitch in a few bucks to help fund Mother Jones' investigative journalism? We're a nonprofit (so it's tax-deductible), and reader support makes up about two-thirds of our budget.

We noticed you have an ad blocker on. Can you pitch in a few bucks to help fund Mother Jones' investigative journalism?