Margot Sanger-Katz writes about the difficulty of choosing a health care plan:

The range of choice is generally heralded as a good thing….But it turns out in real life most people are terrible at picking the health plan that is right for them. Health insurance is a complicated financial product, and study after study has shown that people routinely pick bad plans, even choosing options that leave them worse off financially in every possible scenario.

Needless to say, this is a pretty good argument for universal health care. But let’s put that aside and move on:

But what is the alternative to choice? Amanda Starc, an associate professor of management at Kellogg School of Management at Northwestern University, said there was evidence that people really did want different things from health insurance. About a third of people 65 and older are currently enrolled in private Medicare Advantage plans, a share that is large enough to suggest that many would be less happy with only the choice of government Medicare.

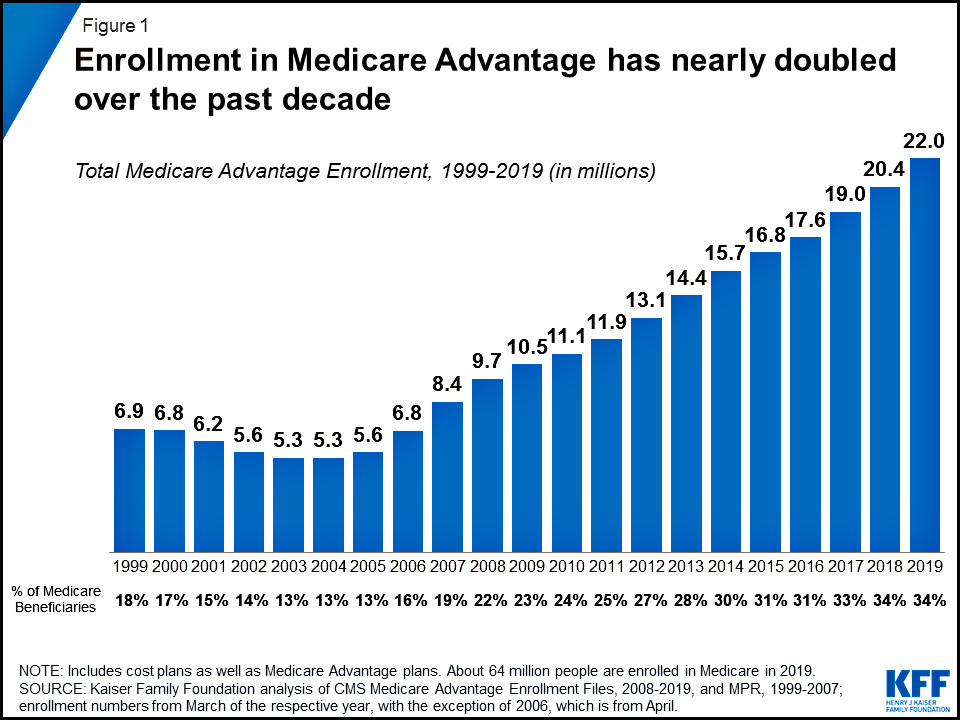

That’s true. Enrollment in Medicare Advantage plans has grown substantially over the past couple of decades:

But why has this happened? Is it because people love choice?

Maybe. But there are other factors at work here. Up through 2010 or so, the federal government reimbursed MA plans at a substantially higher rate than traditional Medicare, which meant that MA plans could afford to be more generous. Obamacare attempted to rein this in, but when you add everything up (reimbursement rates, quality bonuses, lower bid rates, etc.) MA plans were still more generously funded than traditional Medicare even after Obamacare took effect. In other words, people increasingly chose MA plans not because they loved choice so much, but because they were genuinely able to offer better benefits.

They also offered something else that turned out to be highly prized by customers. Here’s the conclusion of a study from the Urban Institute:

Our multivariate analyses found that county-level MA penetration growth was related to access to $0 premium and four-or five-star plans, implying that beneficiaries choose MA more frequently where MA plans are more generous or higher quality. MA plans with a four-star rating or higher have higher benchmarks to bid against and a higher rebate percentage to pass on to beneficiaries through extra benefits, and five-star plans can offer year-round open enrollment. Research shows that $0 premiums and extra benefits feature prominently in MA plan advertising (Cai et al. 2008), suggesting that plans see generosity as a major selling point.

People might like choice, but they like $0 premiums even more! This is pretty popular among Obamacare plans too. This should not come as a great surprise to anyone.