Who would get hurt by the Republican health care plan? The short answer is: pretty much everybody. But Andrew Sprung suggests a more precise way of looking at it, which he calls Total Subsidized Share of Costs, or TSS.

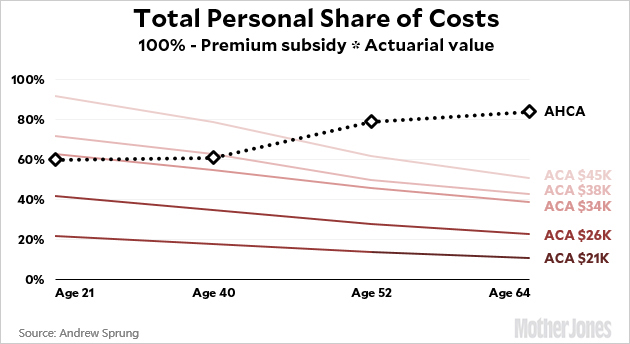

It’s a pretty simple concept. If, say, the government pays half your health care premium, and your policy covers half your medical expenses, then your TSS is the product of those two things: one quarter. The other three-quarters you have to pay yourself. If (more realistically), Obamacare pays 85 percent of your premium, and the policy covers 80 percent of your costs (i.e., it has an “actuarial value” of 80 percent), then your TSS is 68 percent and you pay the other 32 percent. Since CBO calculated actuarial values for the Republican bill, we can calculate TSS for both Obamacare and AHCA.

My purpose on earth is to put other people’s numbers into colorful charts, so let’s do that. But first, I happen to think that a better measure to look at is not how much is subsidized, but how much the covered person has to pay. So instead of TSS, let’s look at the inverse: Total Personal Share of Costs, or TPS.1 Here’s my TPS report for various income levels:

If your income is $34,000 or less, Obamacare is a better deal for everyone. At higher income levels, Obamacare is still better for older people but AHCA is better for young people.

Of course, someone earning $40,000 or more is likely to have a job that provides health insurance, and therefore doesn’t need either Obamacare or AHCA anyway. For nearly all the people who actually need individual health insurance in the first place, the Republican plan is a disaster. Poor people will all pay at least 60 percent of their health care costs, and older people will pay more than 80 percent.

1Astute readers will recognize another reason that I like the acronym TPS.