<a href="http://www.flickr.com/photos/stevendepolo/3125850996/sizes/o/in/photolist-5LdNAG-6RgSdC-9jUHyS-9gn9JE-avP8nX-5YPGro-avP87D-9qBoEw-6N7Wbt-bATN34-bnYWLY-9pidi6-9h5DeH-9d3Vr6-9eLHpZ-9gDKrJ-9fvsRr-9fk3Vq-9gnjgU-9f4dFg-9gAuYi-9i6jMZ-9fh2z4-9kDodH-9gU2w7-9kcBJU-9nKuAM-9fyuAf-9n2eBN-9j7jFL-9i9x8C-9ezmf9-9gDMKq-9fyyto-9hn6zf-9dxk5L-9ntaRH-9mP8hA-9gR4MB-9in4fM-9gQZaV-9f4gPt-9iqeoC-9kSZkx-9fk6Zm-9i6y9v-9niec7-9dxeVS-9hnfrb-9p5ux1-9h8rH3/">stevendepolo</a>/Flickr

This story first appeared on the TomDispatch website.

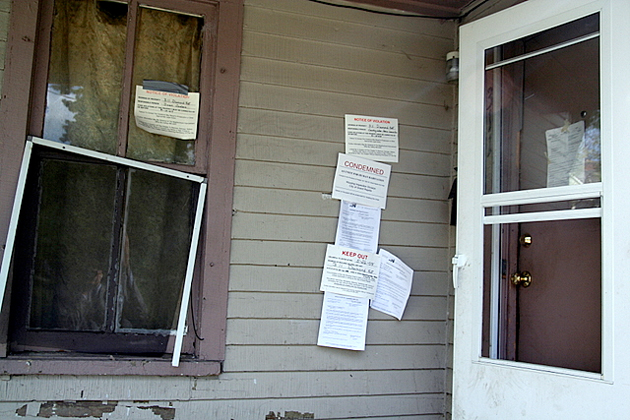

We cautiously ascend the staircase, the pitch black of the boarded-up house pierced only by my companion’s tiny circle of light. At the top of the landing, the flashlight beam dances in a corner as Quafin, who offered only her first name, points out the furnace. She is giddy; this house—unlike most of the other bank-owned buildings on the block—isn’t completely uninhabitable.

It had been vacated, sealed, and winterized in June 2010, according to a notice on the wall posted by BAC Field Services Corporation, a division of Bank of America. It warned: “entry by unauthorized persons is strictly prohibited.” But Bank of America has clearly forgotten about the house and its requirement to provide the “maintenance and security” that would ensure the property could soon be reoccupied. The basement door is ajar, the plumbing has been torn out of the walls, and the carpet is stained with water. The last family to live here bought the home for $175,000 in 2002; eight years later, the bank claimed an improbable $286,100 in past-due balances and repossessed it.

![]() It’s May 2012 and we’re in Woodlawn, a largely African American neighborhood on the South Side of Chicago. The crew Quafin is a part of dubbed themselves the HIT Squad, short for Housing Identification and Target. Their goal is to map blighted, bank-owned homes with overdue property taxes and neighbors angry enough about the destruction of their neighborhood to consider supporting a plan to repossess on the repossessors.

It’s May 2012 and we’re in Woodlawn, a largely African American neighborhood on the South Side of Chicago. The crew Quafin is a part of dubbed themselves the HIT Squad, short for Housing Identification and Target. Their goal is to map blighted, bank-owned homes with overdue property taxes and neighbors angry enough about the destruction of their neighborhood to consider supporting a plan to repossess on the repossessors.

“Anything I can do,” one woman tells the group after being briefed on its plan to rehab bank-owned homes and move in families without houses. She points across the street to a sagging, boarded-up place adorned with a worn banner—”Grandma’s House Child Care: Register Now!”—and a disconnected number. There are 20 banked-owned homes like it in a five-block radius. Records showed that at least five of them were years past due on their property taxes.

Where exterior walls once were, some houses sport charred holes from fires lit by people trying to stay warm. In 2011, two Chicago firefighters died trying to extinguish such a fire at a vacant foreclosed building. Now, houses across the South Side are pockmarked with red Xs, indicating places the fire department believes to be structurally unsound. In other states—Wisconsin, Minnesota, and New York, to name recent examples—foreclosed houses have taken to exploding after bank contractors forgot to turn off the gas.

Most of the occupied homes in the neighborhood we’re visiting display small signs: “Don’t shoot,” they read in lettering superimposed on a child’s face, “I want to grow up.” On the bank-owned houses, such signs have been replaced by heavy-duty steel window guards. (“We work with all types of servicers, receivers, property management, and bank asset managers, enabling you to quickly and easily secure your building so you can move on,” boasts Door and Window Guard Systems, a leading company in the burgeoning “building security industry.”)

The dangerous houses are the ones left unsecured, littered with trash and empty Cobra vodka bottles. We approach one that reeks of rancid tuna fish and attempt to push open the basement door, held closed only by a flimsy wire. The next-door neighbor, returning home, asks: “Did you know they killed someone in that backyard just this morning?”

The Equivalent of the Population of Michigan Foreclosed

Since 2007, the foreclosure crisis has displaced at least 10 million people from more than four million homes across the country. Families have been evicted from colonials and bungalows, A-frames and two-family brownstones, trailers and ranches, apartment buildings and the prefabricated cookie-cutters that sprang up after World War II. The displaced are young and old, rich and poor, and of every race, ethnicity, and religion. They add up to approximately the entire population of Michigan.

However, African American neighborhoods were targeted more aggressively than others for the sort of predatory loans that led to mass evictions after the economic meltdown of 2007-2008. At the height of the rapacious lending boom, nearly 50% of all loans given to African American families were deemed “subprime.” The New York Times described these contracts as “a financial time-bomb.”

Over the last year and a half, I traveled through many of these neighborhoods, reporting on the grassroots movements of resistance to foreclosure and displacement that have been springing up in the wake of the explosion. These community efforts have proven creative, inspiring, and often effective—but in too many cities and towns, the landscape that forms the backdrop to such a movement of hope is one of almost overwhelming destruction. Lots filled with “Cheap Bank-Owned!” trailers line highways. Cities hire contractors dubbed “Blackwater Bailiffs” to keep pace with the dizzying eviction rate.

In recent years, the foreclosure crisis has been turning many African American communities into conflict zones, torn between a market hell-bent on commodifying life itself and communities organizing to protect their neighborhoods. The more I ventured into such areas, the more I came to realize that the clash of values going on isn’t just theoretical or metaphorical.

“Internal displacement causes conflict,” explained J.R. Fleming, the chairman of the Chicago Anti-Eviction Campaign. “And there’s no other country in the world that would force so much internal displacement and pretend that it’s something else.”

Evictions at Gunpoint

It was three in the morning when at least a dozen police cruisers pulled up to the single-story, green-shuttered house in the African American Atlanta suburb where Christine Frazer and her family lived. The precise number of sheriffs and deputies who arrived is disputed; the local radio station reported 25, while Frazer recalled seeing between 40 and 50.

A locksmith drilled off the home’s locks and dozens of officers burst into the house with flashlights and handguns.

“Who’s in the house?” they shouted. Aside from Frazer, a widow with a vocal devotion to the Man Above, there were three other residents: her 85-year-old mother, her adult daughter, and her four-year-old grandson. Things began to happen fast. Animal control rounded up the pets. Officers told the women to get dressed. Could she take a shower? Frazer asked. Imagine there’s a fire in your house, the officer replied.

“They came to my home like I was a drug dealer,” she told reporters later. Over the next seven hours, the officers hauled out the entire contents of her home and cordoned off the street to prevent friends from helping her retrieve her things.

“I have no idea where some of my jewelry is, stuff I bought when I was 30 years old,” said Frazer. “I am sixty-three. They just threw everything everywhere, helter-skelter on the front lawn in the dark.”

The eviction-turned-raid sparked controversy across Atlanta when it occurred in the spring of 2012, in part because Frazer had a motion pending in federal court that should have stayed the eviction, and in part because she was an active participant of Occupy Homes Atlanta. But this type of militarized reaction is often the outcome when communities—especially those of color—organize to resist eviction.

When Nicole Shelton attempted to move back into her repossessed home in a picket-fence subdivision in North Carolina, the Raleigh police department sent in more than a dozen police officers and an eight-person SWAT team. Officers were equipped with M5 submachine guns. A helicopter roared overhead. In Boston, one organizer with the community group City Life/Vida Urbana remembers the police acting so aggressively at an eviction blockade in a Haitian neighborhood that the grandmother of the family had a heart attack right in the driveway.

When Nicole Shelton attempted to move back into her repossessed home in a picket-fence subdivision in North Carolina, the Raleigh police department sent in more than a dozen police officers and an eight-person SWAT team. Officers were equipped with M5 submachine guns. A helicopter roared overhead. In Boston, one organizer with the community group City Life/Vida Urbana remembers the police acting so aggressively at an eviction blockade in a Haitian neighborhood that the grandmother of the family had a heart attack right in the driveway.

And sometimes it doesn’t require resistance at all. On the South Side of Chicago, explained Toussaint Losier, a community organizer completing his Ph.D. at the University of Chicago, “They bust in the door, and it’s at the point of a gun that you get evicted.”

Exiles in America

There have been widespread foreclosures—and some organized resistance—in predominately white communities, too. Kevin Kirkman, captain of the civil division of the Lee County sheriff’s office, explained, “I get so many [eviction] papers in here, it’s unbelievable.”

More than 75% of the residents in North Carolina’s Lee County are whites. But Kirkman still sees the ripple effects of mass foreclosure here. “You’re talking about a mudslide where a lot of things are affected. You’re talking about taxes, about retail sales if people move, about food services, about gasoline. You see what I’m talking about? When you lose a family in the community? Some people leave the community. I have seen people leave the state of North Carolina.”

He added, “I’m going be honest with you, my feeling is that I would not do these evictions.”

Still, the difficulties white America has faced during the foreclosure crisis don’t compare with what Wall Street and the banks have inflicted, physically and psychologically, on African American neighborhoods. As countless leaked documents, insider dispositions, and Department of Justice filings demonstrate, those neighborhoods were systematically and illegally targeted for the worst of the worst mortgages. As one former Wells Fargo mortgage broker explained in a sworn affidavit, “The company put ‘bounties’ on minority borrowers. By this I mean that loan officers received cash incentives to aggressively market subprime loans in minority communities.”

This pushing of predatory loans was all the more insidious because these same communities had been starved of mortgages for decades as a result of the Federal Housing Authority’s refusal to guarantee loans in communities of color. As Mike Fannon, development associate for the Charles H. Wright Museum of African American History in Detroit, explained, “The same banks that denied capital now injected too much toxic capital and decimated the local economy.”

The effect, according to a 2012 National Fair Housing Alliance report, has been “the largest loss of wealth for these communities in modern history.” Between 2009 and 2012 African Americans lost just under $200 billion in wealth, bringing the gap between white and black wealth to a staggering 20:1 ratio.

There is also a longer trajectory of racial exclusion at play here, a history that makes the foreclosure crisis yet another chapter in an epic and enduring quest for home. From enslavement to sharecropping, redlining to restrictive covenants, the United States has too often been an inhospitable land for people of color. Fifty years ago, Martin Luther King echoed W.E.B. Dubois in declaring that the African American still “finds himself in exile in his own land.” Today, it’s hard not to see that reality painted across the 2010 census data, where the maps measuring the concentration of vacant houses and the maps measuring the concentration of African Americans, while not exactly the same, are uncomfortably close to a match.

As Ben Austen wrote in the New York Times Magazine, “The US Postal Service, which tracks these numbers, reported that 62,000 properties in Chicago were vacant at the end of last year, with two-thirds of them clustered as if to form a sinkhole in just a few black neighborhoods on the South and West Sides.” The same phenomenon holds true in cities across the country. And once a house is empty in such neighborhoods, all too often, no one is moving back in.

Crime Starts at the Top

“There were feces in the basement, urine, rolled-up carpet,” said Thomas Turner, a housing activist in Chicago describing the inside of a foreclosed home, once owned, according to neighbors, by an 80-year-old man. Under the ownership of the Pittsburgh-based bank PNC, Turner explained, “It was abandoned for six years, so squatters and strippers had punched holes in the walls. There was no toilet, no tub, all the kitchen cabinets were torn out. The bedroom looked like someone had taken a sledgehammer and just started swinging… I still see gang members on the front porch or rolling up real slow in the car.”

Another Chicago resident, Erica Johnson, described a vacant home similarly. “There were clothes, books, broken dressers, little white drug bags, used condoms,” she said. “It was a little drug house, and they were probably bringing their girls up in here.”

Some foreclosed homes become brothels, such as a Deutsche Bank-owned house in South Los Angeles where the girls’ names and prices were scrawled in blue marker across the upstairs walls. Others become meth labs or gang hideouts.

These bank-owned vacant houses help spread crime and poverty in already distressed communities—a reality that became obvious to me when I accompanied Dorian Morris, a certified building inspector, on one of his surveys of the vacant homes on the north side of Minneapolis. Signs on nearly every home advertised the severity of the housing crisis in this area: neon green “no trespassing” stickers on boarded-up foreclosed homes and red “stand together, stop foreclosure” posters on places supporting Occupy Homes Minneapolis. On more than a dozen lots, the only indication that a family once lived there was a skinny red metal rod marking the spot where a razed house once stood.

As in other hard-hit African American neighborhoods across the country, residents here had organized to stop bank-pursued evictions from stripping the value from the community. Neighborhood support had, for instance, helped a mother named Monique White beat her eviction in a highly publicized six-month battle against US Bank only weeks before I arrived. Still, the never-ending evictions were eating away at the stability of the neighborhood.

“That’s a known crack house,” said Morris, as he pointed at a brick structure less than 100 meters away from a neighborhood park. More than half the homes within sight were boarded up with plywood. Within five minutes, we had passed two former residences he identified as current drug houses and a handful more that he said had already been raided by the police—all foreclosed homes where families used to live.

As we drove, we discussed the illegal chain of events that transformed these homes into drug dens. The crimes started at the top. Banks peddled toxic mortgages like crack, paying employees cash incentives to push them in African American neighborhoods. The loans exploded, so they forged millions of foreclosure affidavits to speed state-enforced evictions.

Once homes are vacant, bank contractors insufficiently seal and maintain them, allowing intruders to strip the houses of their copper wiring, plumbing, and sometimes even the furnace. The copper alone sells for anywhere from 50 cents to a dollar per pound. Finally, people dealing drugs begin to use the houses at night as distribution centers. The street-level crime drags down neighboring property values, spurring more foreclosures and evictions. And so the cycle continues.

Banks are legally obligated to maintain and market their foreclosed properties, but they often shirk those responsibilities—especially in communities of color. In an investigation of more than 1,000 homes across the country, the National Fair Housing Alliance found that bank-owned homes in communities of color were more likely than homes in white neighborhoods to have graffiti and peeling paint on the exterior, trash and dead leaves strewn across the sidewalk, unsecured locks on the doors, and be missing “for sale” signs on their front lawns.

Foreclosed houses in such neighborhoods were also 80% more likely to have a broken or boarded-up window, and 30% more likely to have trash on the front lawn. After a lawsuit, Wells Fargo paid $42 million to settle charges of racially discriminatory maintenance; there’s scant evidence to suggest the practice has changed since. Cities have increased fines levied against banks that don’t maintain their houses, but not a single bank has been held accountable for drug dealing, murders, and rapes that occur on their unmaintained or poorly maintained properties. The only “crime” they appear concerned about is when community activists try to fix up such homes and move families in—doing the job the bank was supposed to do in the first place. Then banks call the police to arrest the “trespassers.”

Sacrifice Zones

The double standards in property maintenance lead to an “extremely troubling” trend in home sales: these uninviting neglected houses, disproportionately located in communities of color, are most often being snapped up by investors rather than families. Overwhelmingly, the investor of choice is the Blackstone Group, one of the world’s largest private equity firms and now the nation’s largest owner of single-family homes. Since April 2012, Blackstone has spent more than $4.5 billion buying at least 30,000 houses concentrated in cities hard-hit by foreclosure, including Atlanta, Jacksonville, Orlando, Chicago, Charlotte, Phoenix, and urban areas across California. According to local real estate brokers, the company often makes its purchases in cash.

The idea is that there’s big money to be made in rental properties these days, given that there are millions of displaced, former homeowners with wrecked credit scores looking for places to stay. It’s like a pay-to-play game of musical chairs—except Wall Street owns the stereo, the speakers, the chairs, and the roof, and somehow when the music stops you’re always out.

Vacant houses, whether owned by banks or Blackstone, create foreclosure spirals, each vacant house dragging down the property values of neighbors, which, in turn, decreases a city’s property tax revenue and the capacity of local government to provide essential services. Shuttered schools in Philadelphia and Chicago. Closed hospitals in Cleveland. Slashed senior programs in Baltimore. All of these essential services, eliminated far more often in communities of color, are the collateral damage of the foreclosure crisis.

A 2011 report by the US Government Accountability Office, submitted to the House Subcommittee on Regulatory Affairs, cited nearly a dozen examples of how such declines in tax revenues caused by vacancies have led cities to cut funding for public works, libraries, parks, recreation programs, and school districts. One city even cut a program intended to address vacant foreclosed properties, thanks to a tax revenue shortfall.

The final dystopian outcome of this spiral is what journalist Naomi Klein famously termed the shock doctrine: a crisis is pushed so far that it finally justifies dramatic outside intervention (read: privatization). It’s the type of outcome we’re currently seeing in Michigan, where, according to a court ruling last week, “Detroit’s recent bankruptcy filing only emphasizes the broader consequences of predatory lending and the foreclosures that inevitably result.” That city may be undergoing the largest municipal bankruptcy in US history, but unlike when the big banks and giant financial outfits teetered at the edge of collapse, President Obama has made it clear that this time there will be no billion-dollar federal bailout.

“With the mass displacement, it ends up being a situation where people are just like, ‘Well, we’ll just have to bulldoze those homes,'” Chicago organizer Toussaint Losier told me. “They become sacrifice zones rather than places where people bring imaginative solutions.”

The Shield and the Sword

Small groups of community organizers are shouldering the Herculean task of protecting such neighborhoods abandoned by the federal government.

“Look, if you want to take our home, it’s an act of war,” explains Losier, so his group’s response is, metaphorically, “the sword and the shield.” It’s a strategy he learned from the Boston anti-foreclosure group City Life/Vida Urbana. The shield represents the exceedingly modest legal protection afforded to people under a judicial system that assigns more rights to the banks than them—and allows no-guilt settlements for the powerful caught flagrantly breaking the law. (In the case of foreclosure crimes, see for example the $335 million Bank of America discrimination settlement in 2011, the $26 billion robo-signing settlement in 2012, and the $8.5 billion settlement over wrongful foreclosures in 2013.)

The sword represents actions—from petitions to eviction blockades—aimed at stopping evictions and repairing neighborhoods. And yes, there is a life-size, fabricated sword-and-shield set at the City Life office in Boston. First-time attendees of the group’s weekly meetings must hoist the sword over their heads and assert that they are willing to fight for their homes. “Then we will fight with you!” the rest of the group cheers.

Across the country, communities of color deploy these two strategies, and a third that could be called “the paintbrush”: creative tactics aimed at building something new amid the devastation. In Detroit and Philadelphia, neighborhoods are seeding community gardens in hundreds of vacant lots. In Boston, one set of community activists cleaned up their block and dumped the trash—gathered from the front lawn of a foreclosed Bank of America-owned home—on the doorstep of the regional bank president’s brownstone.

In Minnesota and California, grassroots political organizing pressured state legislatures to adopt the nation’s first two homeowner bills of rights. A Barclays report later complained that “servicers have become significantly more cautious when carrying out foreclosure sales” as a result of the legislation. In Chicago, home liberation groups are rehabbing and occupying vacant properties, while anti-violence groups are intervening in the conflicts caused by poverty and mass displacement.

Both of the foreclosed Chicago houses that Thomas Turner and Erica Johnson described as being filled with feces, used condoms, and drugs are now clean, painted, and occupied. Turner even stenciled small purple birds on the walls of the one he worked on. But the continued scale of the crisis—forgotten by a media more interested in rising home values than eviction notices—requires more than community rehab and tepid financial regulation. It demands that we question, and reimagine, a system of property ownership that has prevented large segments of the population from making real decisions about the communities in which they live. And in case you’re thinking that this is a problem only for Black America, think again. As the New York Times warned in April, “The alchemists of Wall Street are at it again… reviving the same types of investments that many thought were gone for good.”

The question is whether, this time around, we’ll see their potion for what it is: poison that threatens to turn each of us, as W.E.B. Dubois wrote, into “an outcast and a stranger in my own house.”

Laura Gottesdiener is a journalist, social justice activist, and author of A Dream Foreclosed: Black America and the Fight for a Place to Call Home, published this month by Zuccotti Park Press. She is an associate editor for Waging Nonviolence, and she has written for Rolling Stone, Ms. magazine, the Arizona Republic, AlterNet, and other publications. This is her first TomDispatch piece. She lived and worked in the People’s Kitchen during the occupation of Zuccotti Park.

Follow TomDispatch on Twitter and join us on Facebook or Tumblr. Check out the newest Dispatch book, Nick Turse’s The Changing Face of Empire: Special Ops, Drones, Proxy Fighters, Secret Bases, and Cyberwarfare. To stay on top of important articles like these, sign up to receive the latest updates from TomDispatch.com here.