In the New York Times this weekend, Gretchen Morgenson and Louise Story write about how Goldman Sachs both helped along the collapse of AIG and profited from it at the same time. Basically, Goldman acquired lots of mortgage-backed securities they thought were likely to tank, then bought CDS contracts from AIG to insure against that decline. summarizes the rest:

In the New York Times this weekend, Gretchen Morgenson and Louise Story write about how Goldman Sachs both helped along the collapse of AIG and profited from it at the same time. Basically, Goldman acquired lots of mortgage-backed securities they thought were likely to tank, then bought CDS contracts from AIG to insure against that decline. summarizes the rest:

- When Goldman’s investments declined, they submitted insurance claims for the losses, but insisted on determining the amount of their damages on their own, without any input from AIG, any auditor or the market.

- After Goldman got as much money out of AIG as they thought they could, their stock analysts issued a report about how AIG was bleeding cash and their creditors wouldn’t negotiate, without mentioning that AIG was bleeding cash because of them and that Goldman was the creditor that wouldn’t negotiate. AIG’s stock tanked.

- The government stepped in, took an 80 percent share in AIG and then paid Goldman and the other creditors all the money they’d asked AIG for at the start of the negotiations in 2007, without using their power to force AIG’s creditors to negotiate.

Given the scope of AIG’s problems, I guess I doubt if any of this really mattered in the long run. AIG was going to collapse no matter what Goldman did or didn’t do, so in a sense this is a bit of sideshow. But then there’s this:

When the federal government, including then-Treasury Secretary Hank Paulson (who once served as chairman and CEO of Goldman Sachs), directed AIG to pay Goldman exactly what it wanted, it overrode significant and long-standing misgivings by AIG’s lawyers and accountants that Goldman’s estimates of its losses were correct. Morgenson and Story note that the prices on the very securities for which Goldman demanded insurance payments have since rebounded — but under the terms of the deal struck by the federal government, Goldman doesn’t have to pay a cent of its insurance settlement back to either AIG or the taxpayers. That’s quite the sweetheart deal for Goldman Sachs, if not taxpayers.

Now, of course, the question is what did Tim Geithner know about this and when did he know it? That story is still developing.

I talk about leverage as the source of all evil in the financial sector fairly frequently, but it’s been a while since I’ve had a post reminding everyone about the tax treatment that makes debt so attractive. Today,

I talk about leverage as the source of all evil in the financial sector fairly frequently, but it’s been a while since I’ve had a post reminding everyone about the tax treatment that makes debt so attractive. Today,  his political instincts are the right ones. Maybe he understands better than me that the public needs to see graphically that Democrats did everything they could to work with the GOP and were completely rebuffed. Maybe.

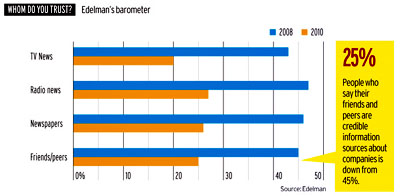

his political instincts are the right ones. Maybe he understands better than me that the public needs to see graphically that Democrats did everything they could to work with the GOP and were completely rebuffed. Maybe. AdAge reports that Edelman’s “Trust Barometer” has grim news: we don’t trust much of anybody anymore when it comes to product and company recommendations.

AdAge reports that Edelman’s “Trust Barometer” has grim news: we don’t trust much of anybody anymore when it comes to product and company recommendations.  have been common knowledge for a long time and haven’t changed a whit in the past year. The other causes of the deficit — Bush-era tax cuts, Bush-era war spending, Bush-era Medicare expansion, and a Bush-era recession — are also common knowledge. And the global recession makes short-term deficits far more defensible than they ever were under Bush.

have been common knowledge for a long time and haven’t changed a whit in the past year. The other causes of the deficit — Bush-era tax cuts, Bush-era war spending, Bush-era Medicare expansion, and a Bush-era recession — are also common knowledge. And the global recession makes short-term deficits far more defensible than they ever were under Bush. I haven’t been following in detail the various recent disputes about specific global warming claims, but if Walter Russell Mead is to be believed,

I haven’t been following in detail the various recent disputes about specific global warming claims, but if Walter Russell Mead is to be believed,  If you hate Rahm Emanuel — and I know lots of you do — you’re going to love Edward Luce’s Financial Times piece that blames Barack Obama’s reliance on a small inner circle of aides for his

If you hate Rahm Emanuel — and I know lots of you do — you’re going to love Edward Luce’s Financial Times piece that blames Barack Obama’s reliance on a small inner circle of aides for his