Obamacare’s moment of truth is coming. By now we’ve heard all the scare stories about a few health insurers in a few states requesting gigantic rate hikes for next year. But over the next few weeks, states are going to start publishing the actual average rate increases that consumers will see in 2016. California released its report today. It’s still marked preliminary, but you can expect that the final numbers will be very close to these:

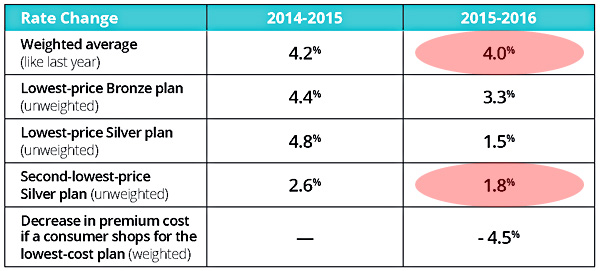

I’ve highlighted two numbers. First, the overall average rate increase is 4.0 percent. That’s way lower than you’ve seen in the scary headlines. And this is for a state that makes up more than a tenth of the country all by itself.

Second, the price of the second-lowest-price silver plan has gone up 1.8 percent. This is the figure used to calculate subsidy levels, so it’s an important one. In fact, here’s an interesting consequence of that number: because subsidies will be going up roughly 1.8 percent, and the cost of the lowest-price silver plan is going up only 1.5 percent, the net cost (including subsidies) of buying the cheapest silver plan is actually going down. As you can see in the bottom row, if you shop for the lowest-priced plan, your premiums are likely to decrease about 4.5 percent.

I have a feeling this number is not going to be widely reported on Fox News.

Now, California isn’t necessarily a bellwether for all the other states. Because it’s the biggest state in the union, it has lots of competition that helps drive down prices. A big population also means less variability from year to year. Also: California’s program is pretty well run, and the California insurance market is fairly tightly regulated. All this adds up to a good deal for consumers.

In any case, the headline number here is a very reasonable 4 percent increase in overall premiums, and a 4.5 percent decrease for consumers shopping for the cheapest plans. These are real statewide numbers, not cherry-picked bits and pieces designed to encourage hysteria. Once again, it looks like Obamacare is working pretty well.

This all comes via Andrew Sprung, who has much more detail here.