These are the islands of Deenish (left) and Scariff (right). The picture was taken near the Coomakista Pass, on the Ring of Kerry between Caherdaniel and Waterville. If you judge scenic points by the size of the turnout provided for cars and tour buses, Coomakista is by far the biggest attraction in these parts.

There’s a statue of Mary at Coomakista, so I vaguely assumed that “kista” meant Christ. But vague assumptions aren’t enough for this blog, so I looked it up. This turned out to be surprisingly hard, but as near as I can tell, a coom is a hollow and kista means treasure or somesuch. According to the Irish Times, “The placename Coomakista, which means ‘the coom of the cash’, stems from a legend that 18th century French privateers stashed money in the mountain recess.”

In any case, it really is a stunning view, and it changes subtly every day depending on the weather. And yes, I do have a picture of the Madonna statue! You’ll see it one of these days.

We’re going to bring the individual rate to 10 percent or 12 percent, much lower than it is right now.

Boo yah! This would be quite a cut from the current top rate of 39.6 percent. Even Grover Norquist doesn’t dream of tax rates like this. That means it’s time for another round of “WTF was he talking about?” Let’s review our options:

It was just a slip of the tongue. But this is unlikely since Trump specifically said “10 or 12.” He really meant it.

He’s talking about personal income tax as a percentage of GDP, and he wants to increase it to 10 or 12 percent. But no: he said it would be “much lower” than it is right now.

He was talking about the log of the root mean square of the average tax paid by people in the top bracket.

He has no clue what he’s talking about.

Hmmm. I think I’m going with Option 4. The Post phrased this diplomatically: “It wasn’t clear exactly what he was referring to and the White House didn’t immediately clarify his intention.”

No worries, though, I’m sure the White House will explain things soon. There’s probably already some poor schmoe staying up all night looking for something—anything—that the Republican plan will plausibly reduce to 10 or 12 percent.

Here’s a hint: adjusted gross income. Currently, individual income taxes are about 14 percent of reported AGI. A tax plan that reduced this rate to “10 or 12” percent would represent a tax cut of 15-30 percent. That’s the ticket, I think.

Alternatively, the White House could just invent some new numbers of their own. Or declare that the press is playing “gotcha games.” Or insist that the president can say whatever he wants, and Beltway elites will never stop him from talking directly to the common man. Or claim ignorance until reporters get tired of asking. All of these have worked well for them in the past.

POSTSCRIPT: The Post also reports that Republicans are “looking for a way to keep their plan from being a massive windfall for the wealthiest Americans.” Hahahaha. Sure they are. DC journalists crack me up sometimes.

President Trump has issued a new travel ban that bars travel completely, not just for 90 days. So why will this one pass court muster when the old one didn’t?

Officials said his new action was the result of a deliberative, rigorous examination of security risks that was designed to avoid the chaotic rollout of his first ban. And the addition of non-Muslim countries could address the legal attacks on earlier travel restrictions as discrimination based on religion.

Now we’re talking! Trump has taken my advice and added a couple of non-majority-Muslim countries (North Korea and Venezuela) so that nobody can say this is just anti-Muslim bigotry. I especially think the addition of North Korea is a nice touch. Do we get any non-diplomatic visitors at all from North Korea?

I assume this is going to court more or less instantaneously. We’ll soon see what happens to Travel Ban 3.0.

Real wages for nonsupervisors, which take inflation into account, topped $22 an hour this year, the best inflation-adjusted reading since January 1973,¹ according to Labor Department data. The nonsupervisory figure covers about 70% of the workforce and excludes managers who are more likely to receive bonuses, stock options and other forms of nonwage compensation.

Translation: wage growth for ordinary workers has been so bad that it’s taken 44 years to finally catch up to the levels of 1973.

The article goes on to talk about wage growth during this recovery compared to past recoveries, but you really need to see the whole picture in one place to understand what’s going on. Here it is:

Roughly speaking, the years from 1978 to 1995 were a horror show. During that 17-year period, wages dropped by 15 percent, or 0.9 percent per year. Since then, however, wages have grown steadily. In the 22 years from 1996 to 2017, wages have increased 18 percent, or about 0.9 percent per year.

This is what makes the whole “economic anxiety” interpretation of the 2016 election so peculiar. In 1992, workers had been getting stiffed for over a decade, and winning a campaign by appealing to this hardship made sense.

But in 2016? Wages have bounced around a bit, but basically workers have been making steady gains for over two decades. In particular, between 2012 and 2016 wages rose a healthy 1.35 percent per year—one of the country’s best 4-year periods since the late 60s—and the unemployment rate dropped more than three points. It’s easy to argue—and I do!—that worker gains should have been even higher, but it’s hard to argue that ordinary workers have been in such dire straits that they were willing to vote for anyone who promised to look out for them.

At the same time, there’s little evidence that racism had any more effect on the 2016 election than it did on previous elections. That’s not for lack of trying on Trump’s part, but the white vote has been reliably Republican at about the same level for three decades.² The deplorables who voted for Trump all voted for Bush and McCain and Romney too.

So what’s left? Not much except for James Comey’s letter re-opening Hillary Clinton’s email case. Even with that, Clinton still outperformed the fundamentals. Without it, she would have won.

¹Actually, I think this ought to be January 1974, but what’s a year between friends?

²Except for 1992 and 1996, when Ross Perot split the conservative white vote.

I’ve been playing around with the time-lapse feature on my camera, which turned out to be pretty easy. Then I had to find a video editor for idiots—and learn how to use it—which turned out to be pretty hard. But I persevered! So here you go. This was taken from the backyard of our vacation home a few days ago.

I’ve been playing with the camera again. I finally figured out how to use the panorama mode, which for some reason never seemed to work at home. So here’s a w-i-i-i-i-de angle version of the view from our backyard this morning. If you squint, you can see Marian in the sun room.

My guess is that Trump is trying to goad Kim Jong-un into doing something provocative enough to justify a US attack. In fact, this is so obvious that I have to wonder what South Korea really thinks of Trump’s little twitter war. After all, they’re the ones in danger if Kim retaliates, not us.

Alternatively, of course, Trump tweeted this because he’s a childish buffoon who has no self-control and engages in schoolyard taunts with anyone he doesn’t like. That’s certainly the default explanation for most of what he does.

I don’t know. I just don’t know. Trump speaks, and all the rest of are forced to talk about whatever he wants us to talk about.

This weekend’s big news (so far) is that President Trump blasted Colin Kaepernick at a rally in Alabama and disinvited the Golden State Warriors from a White House visit after Stephen Curry said he wasn’t sure he wanted to go. It escaped nobody’s attention that both of these folks are black. Meanwhile, Jimmy Kimmel—who is extremely white—has been on a multi-day rant against Trumpcare, but has entirely avoided any insults from the president.

In the non-sports world, we have this:

In 2010, Pres. Obama sent 19 navy/USCG ships, inc. a carrier to help after a quake in Haiti. What about >3 million Americans in Puerto Rico?

If there’s anyone in America who needs more help after a natural disaster, it’s hard to think of who it might be. Puerto Rico is poor, deep in debt, and has been almost destroyed by recent hurricanes. So far, though, Trump has mostly limited himself to a tweet saying that he’s totally got Puerto Rico in his thoughts.

But then, they’re just a bunch of Spanish speakers. Not real Americans like the ones in Houston and Tampa, amirite?

The fact that there’s a core of voters in America who actively support this kind of wink-wink white racial politics isn’t surprising. It’s deplorable, but not surprising. Nor is it even that surprising that we have a commander-in-chief willing to base his presidency on explicit appeals to these voters.

But how can Republicans continue to ignore this? I’m not naive about Republican history on this subject, nor about the realities of party politics. And I get that Trump’s outbursts might even be politically helpful for Republicans.¹ But there must be some point where he goes too far for at least a few of them. Right?

On the bright side, as long as Trump is insulting black athletes, at least he’s not risking nuclear war. I guess that’s a positive development.

¹As Steve Bannon said about Democrats, “the longer they talk about identity politics, I got ’em. I want them to talk about racism every day. If the left is focused on race and identity, and we go with economic nationalism, we can crush the Democrats.”

Is this true? It might be. Unfortunately, it’s hard to say.

A couple of days ago I posted a long-exposure shot of a tiny little waterfall. The long exposure gives the water a velvety texture that long ago became a photographic cliche. You see it a lot in “Serenity” posters and the like.

But as you know, I like photographic cliches. In Southern California that means lots of sunsets, because we have pretty good sunsets there. Ireland doesn’t. The air is just too damn clean. That’s why you haven’t seen an Irish sunset from me yet.¹

Waterfalls are just the opposite. We don’t have a lot of those in Southern California, but you can hardly swing a dead sheep in Ireland without hitting one. So here’s another one: the Torc Waterfall, which is part of the Owengarriff river just before it empties into Muckross Lake. This time you get two views: an ordinary shot on the left and a long exposure on the right:

As I mentioned the other day, the big problem with the long-exposure picture is that it uses a long exposure. It takes about eight seconds to get the velvet effect, and since a typical exposure in daytime is around 1/500th of a second, this means the camera is getting about 4000 times more light than usual. That’s tough to deal with. I can usually drop my ISO setting a couple of stops, and reduce my aperture a couple of stops too. I can also apply a 64x neutral density (gray) filter. Altogether, that reduces the light coming into the camera by about 1000 times. So I’m still overexposed by 4x. Or even more if the sun is shining brightly.

This can be fixed in post-processing, but only up to a point. And it does change the look of the photo. Still, as you can see above, it doesn’t change it too much. In fact, depending on the setting and on your taste in photos, it can actually improve things sometimes.

Here’s another one. It’s a little downstream of the waterfall, and both pictures were taken from the exact same spot:

Anyway, that’s that. I happen to really like long exposure water pictures, and since I don’t get much chance to take them at home I’ve been making up for it here. I’ll post all of them at some point, but I’ll spare you any more for the next few weeks. Probably. After all, I’ve taken about 3,000 photos so far, so I have plenty of other good stuff to put up.

¹But I’ve got one or two good ones. Don’t worry. You’ll see one of them eventually.

While Kevin’s on vacation, we’ve invited other Mother Jones writers to contribute posts.

Some of you probably saw my post about the frustrations I encountered trying to freeze my credit with the Big Three. From the feedback, it sounds like some of you aren’t experiencing problems but others haven’t been so lucky. In any case, I’ve got something new to pule about.

After freezing my credit with Equifax, Experian, TransUnion, and small fry Innovis, I figured I should review my various credit reports to make sure there weren’t any weird requests or new accounts in there—especially given that Equifax waited so long to tell the public that hackers may have accessed our social security and credit card numbers and other personal information crooks can use to hijack our identities.

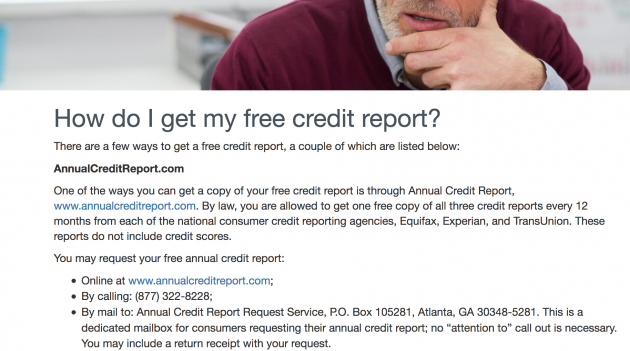

This is supposed to be a freebie. The Fair Credit Reporting Act, originally enacted in 1970, was amended in 2003 to require that the credit-reporting agencies give consumers a chance to review their credit files free of charge and dispute erroneous information in those files that might affect a person’s credit score—and thus their ability to secure a loan at a reasonable price. Each agency, upon request, has to provide you with a free credit report every 12 months. There are numbers you can call, or you can supposedly access free reports from the Big Three via a special website, AnnualCreditReport.com.

But it seems like not all of the agencies want you to find that site. Equifax, to its credit, is pretty straightforward. Google “equifax free credit report” and here’s the first result you see:

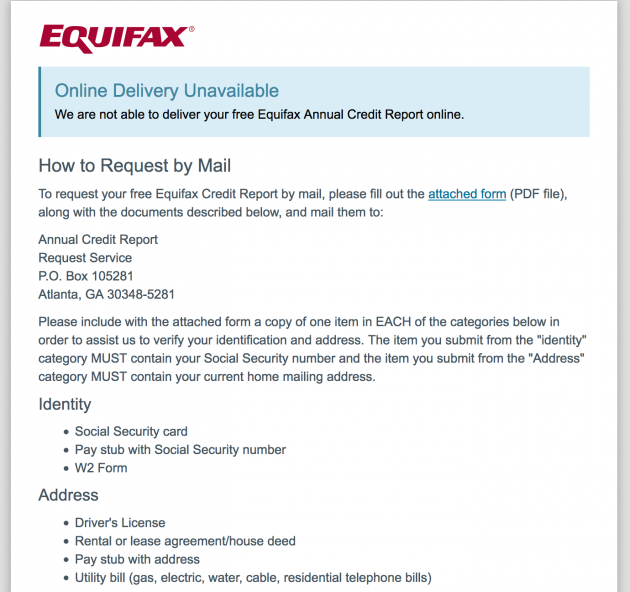

Which takes you to this page:

This is as it should be. The company points you unequivocally to AnnualCreditReport.com. But after going to that site, completing the process, and reviewing and saving PDFs of my credit reports for TransUnion and Experian, Equifax disappointed…

Swell. Having apparently reverted to the dark ages as a result of the Big Hack, Equifax now wants me to send them, by the highly secure medium of snail mail, things any identity thief would love to get his clammy little hands on. I don’t even have the words to… well, I do, but I won’t repeat them here, because your children could be reading over your shoulder.

Innovis, a newer, smaller player, doesn’t use AnnualCreditReport.com. It has you fill out a brief form online and promises to send a copy of your report by mail within a few days. Which is fine, so long as they come through. I’ll let you know if they don’t.

Experian and TransUnion will give you that free credit report if you actually make it to AnnualCreditReport.com. But both companies have come up with ways to turn this very reasonable corporate obligation into a revenue stream.

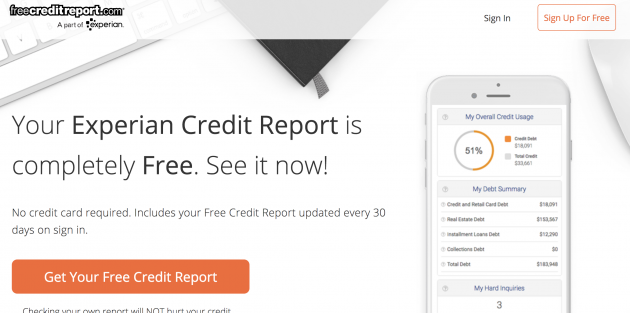

Try Googling “experian free credit report.” The first search results I saw were ads from Experian and FreeCreditReport.com—which is also Experian. I clicked on the first one, and this is where it took me:

They’re offering to give you your credit report and score for a buck. That’s almost free, right? Click on the purple button, and you’ll be sent through an enrollment process. But if you do that without reading the “Important Information” bit underneath, you may not realize you’re signing up for a seven-day trial membership in a $21.95/month service called CreditWorks Plus, which they will then bill you for unless you cancel within those seven days. This comes up again in the fine print during the enrollment process, but who reads fine print?

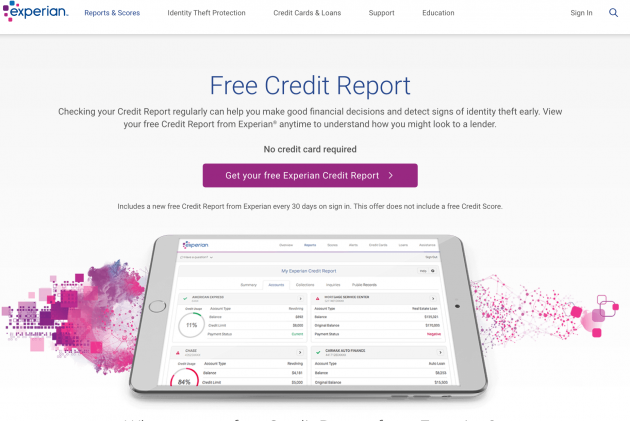

Clicking on the second ad gets you here:

Now it’s free! Clicking on that orange button takes you to a similar enrollment page where you have to give them lots of information (including your social) and agree to epic terms of service that go on for pages and pages. (I didn’t do this because, frankly, it creeped me out.) The service you’re signing up for here, “CreditWorks Basic,” is indeed free, an Experian spokeswoman confirmed via email. “However, we may conduct different offers as well as deploy different offers with partners.”

Let’s have a look at the first non-ad result that came up in my search:

That looks exactly like what we want, right? But the link takes you here:

That purple button again leads to the enrollment process for CreditWorks Basic. Enroll and you become a fresh sales lead for Experian and its affiliates—whose ultimate goal is to convert you into a paying customer.

Let’s step back to that $1 credit report offer. If you poke around on the website of the Better Business Bureau and consumer sites such as ConsumerAffairs.com, you’ll come across a ton of complaints from people who clicked on that big orange button without reading the “Important Information,” and who feel they were suckered. On July 14 of this year, “Terry of Clarkstown, MI” wrote: “Someone needs to do something about this company intentionally deceiving people. I too paid $1.00 for a credit report but instead they signed me up at $21.99 a month. I wasn’t even able to cancel my subscription without paying a $50 balance…” A couple of weeks later “Andy of San Mateo” chimed in: “I paid $1 dollar for a credit score report. I did not realize I signed up for a monthly service with recurring charges in the amount of $21. It is a very dishonest tactic…”

Asked about this common misunderstanding, a spokeswoman responded in an email that Experian discloses its trial offers “clearly and conspicuously” in several locations, and adds that it takes consumer concerns seriously. “As with any large-scale enterprise, there may be a small subset of consumers who are unsatisfied,” she wrote. “When brought to Experian’s attention, the company tries to resolve concerns to the customer’s satisfaction.”

Okay, but is Experian deliberately diverting people who are looking for the free credit report the law guarantees them—the one with no strings attached—to try and sell them paid services? (Not like this is illegal; it just smells a bit.) The spokeswoman didn’t dispute this. She simply noted that the services Experian is selling gives customers more than just a credit report.

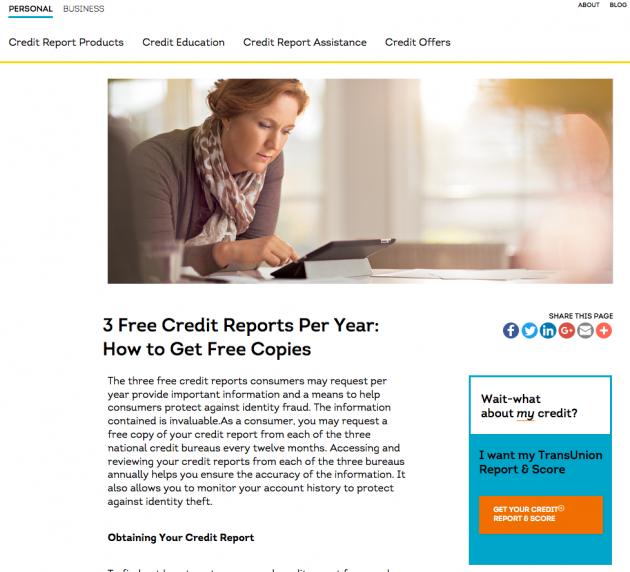

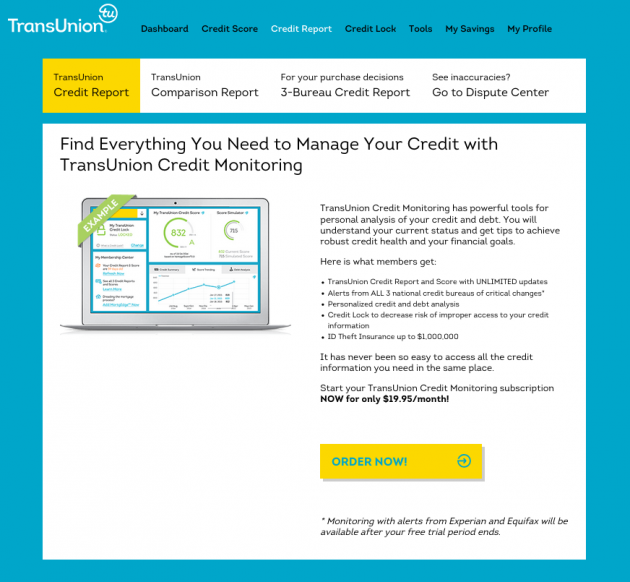

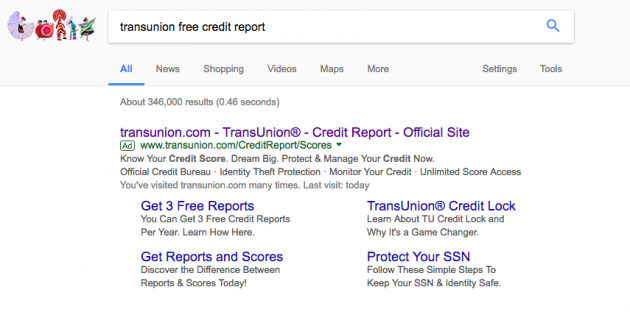

Now let’s look for our free TransUnion credit report. When I Googled “transunion free credit report,” the first result was this TransUnion ad:

Three free reports! That sounds good. We click, and…

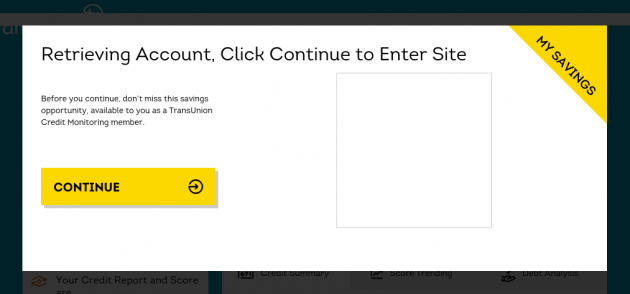

You don’t want a reading assignment, just that free report. So you click on the good ol’ orange button: “Get your credit report and score.” It directs you to a page where you can register or log in.

The TransUnion registration, which I had to do earlier to freeze my credit file, is a minor pain in the butt—they ask security questions that you’ll probably have to dig into your filing cabinet to answer, and you have to agree to an absurdly broad (and probably unenforceable) liability waiver written in all-caps legalese—but you do it anyway. You log in, and here’s what you see:

Um…okay. You click “continue,” and…

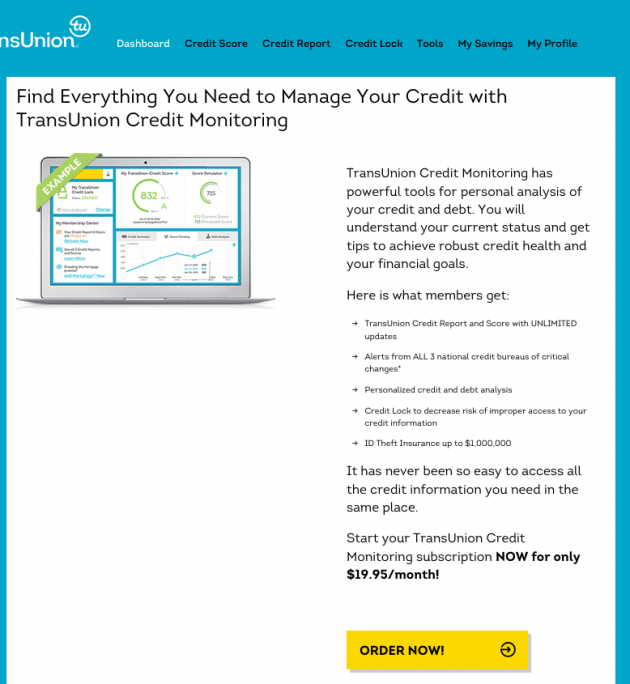

So they’re trying to sell you something, too. Everyone wants to sell, but you just want the free report the ad seemed to be promising. Confused, you lash out at the toolbar menu up top, and select “Credit Score.”

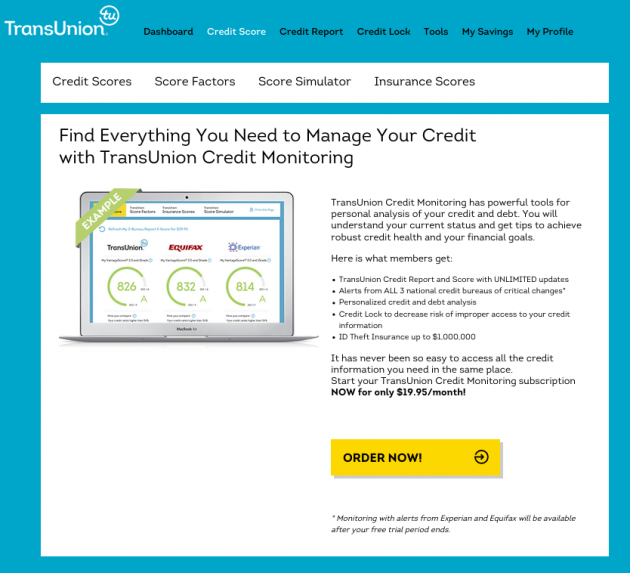

Hey, where have you seen that page before? You try another toolbar option, “Credit Report,” and…

The FREE ONE, MAN! How do we get the FREE ONE?

Oh. Back on that page with the orange button (there are actually three orange buttons; you can only see one of them in my screenshot), if you read down to the second section, it does mention that you can access your credit report at AnnualCreditReport.com. Of course, TransUnion didn’t bother to link up that URL, so you saps will just have to copy and paste it into your browsers. (Did TransUnion’s media representative respond to my inquiries about this wild goose chase? He did not.)

The upshot: If you really want the free one, click here. You only need to put in your information once and nobody will try and pull a fast one on you. Equifax will pull a slow one, but that’s another matter.

Can you pitch in a few bucks to help fund Mother Jones' investigative journalism? We're a nonprofit (so it's tax-deductible), and reader support makes up about two-thirds of our budget.

We noticed you have an ad blocker on. Can you pitch in a few bucks to help fund Mother Jones' investigative journalism?

We’re halfway there, but time’s running out.

With only days left in 2025, we've made real progress toward our $400,000 goal—the funding we need to keep our nonprofit newsroom running at full

strength. But to close the remaining $200,000 gap before December 31, it will take a huge surge in reader support. Whether you've given before or this is your first time, your contribution right now will matter. Will you help us get there?

We’re halfway there, but time’s running out.

With only days left in 2025, we've made real progress toward our $400,000 goal—the funding we need to keep our nonprofit newsroom running at full

strength. But to close the remaining $200,000 gap before December 31, it will take a huge surge in reader support. Whether you've given before or this is your first time, your contribution right now will matter. Will you help us get there?

Which takes you to this page:

Which takes you to this page:

Three free reports! That sounds good. We click, and…

Three free reports! That sounds good. We click, and…